- InGeniusly Speaking

- Posts

- 13.03%

13.03%

By Jeff Walton & Kelly Guest

Where were you when the Miracle on Ice happened? Mortgage interest rates were 13.03% according to Freddie Mac's historical data, which is a far cry from 6.01% yesterday when Team USA sent Canada packing with their maple leaves tucked between their legs. TransUnion's 2026 originations forecast is smattered with double-speak, but let's hope their numbers erred on the conservative side. Builders are a bit sullen, but perhaps the optimism and enthusiasm we saw at IMB 2026 will manifest in a busy spring market.

Table of Contents

CHATTER

Bolstering Banks

Fed Gov Wants More Mortgages to Banks: Bowman Speech at American Bankers Association

In 2008, banks originated around 60% of mortgages and held the servicing rights on about 95% of mortgage balances. Since that time, the contraction has been extraordinary. As of 2023, banks originated only 35% of mortgages and serviced about 45% of mortgage balances.

This out-migration of origination and servicing has been costly for banks, consumers, and the overall mortgage system. In part, this results from over calibration of the capital treatment for these activities, resulting in requirements that are both disproportionate to risk and that make mortgage activities too costly for banks to engage. I see a path forward that incorporates both renewed bank participation in the mortgage market and a safe and sound banking system.

The proposed path forward is shifts in the Basel III capital changes that could make MSRs more attractive to banks.

MBA statement in support of Bowman’s plan to take comments and offer proposals for review.

Crypto’s Coming: NMP Article on How Lenders are Accommodating

A couple ways lenders are moving forward:

Integrating eligible cryptocurrency holdings into non-agency underwriting framework, to allow borrowers to use digital assets for qualification without selling them.

Allowing borrowers to count a portion of Bitcoin and Ethereum toward reserve requirements without liquidation.

CFPB Considerations: HW Article Looks at Differing Opinions

A Council of Economic Advisers posits that the costs imposed on consumers exceed the CFPB’s reported figure of $21B returned to consumers through enforcement actions.

The article quotes other experts who question the CEA’s methodology and argues the consumers who are “paying for CFPB-imposed costs” are high risk borrowers who would be paying more anyway.

Another quote from the Center for Responsible Lending argues that the CFPB regs provide guardrails to prevent a repeat of the 2008 financial crises that cost the country across the board.

Citizens Only

Eliminating a Loophole: HUD Says No Coattail Riders in Subsidized Housing

Secretary Scott Turner announced a new proposed rule to require proof of U.S. citizenship or eligible status for every resident in HUD-funded housing, including “mixed status households.” With this proposed rule, HUD will ensure that taxpayer-funded housing benefits only go to American citizens and eligible individuals for the first time in history.

“Under President Trump’s leadership, the days of illegal aliens, ineligibles, and fraudsters gaming the system and riding the coattails of American taxpayers are over. HUD’s proposed rule will guarantee that all residents in HUD-funded housing are eligible tenants. We have zero tolerance for pushing aside hardworking U.S. citizens while enabling others to exploit decades-old loopholes.”

HUD's proposed rule will close loopholes and prohibit HUD funding from benefitting illegal aliens and ineligible noncitizens who reside in taxpayer-funded housing.

A Spin Doctor Helped with This: TransUnion's 2026 Originations Forecast

The headline says, “TransUnion 2026 Originations Forecast Shows Continued Positive Momentum Amidst Moderate Expansion.” TU predicts a 4% increase in purchase mortgages and a 4.2% increase in refis this year.

“After several years marked by credit behaviors influenced by stubbornly high inflation and elevated interest rates, we may be seeing signs of a return to more traditional growth. As these more typical patterns return, it’s more important than ever for lenders to leverage advanced tools, including trended data, to more accurately assess evolving risk profiles.” - Michele Raneri, vice president and head of U.S. research and consulting at TransUnion.

Smart Certification: Fairway Home Mortgage Partners with Financial/Insurance Industry

Fairway Home Mortgage and the National Association of Insurance and Financial Advisors (NAIFA) today announced a new strategic education partnership to launch the Certified Home Equity Advisor (CHEA) credential: a first-of-its-kind program designed to help financial and insurance professionals responsibly integrate home equity into comprehensive retirement planning.

Developed and delivered in partnership with Fairway Home Mortgage, the CHEA program is taught by licensed reverse mortgage specialists and emphasizes suitability, disclosure, and coordination with broader financial plans — not product sales.

"Housing wealth is one of the largest and most underutilized assets in retirement planning. The CHEA credential reinforces NAIFA's commitment to ethical, client-first education by equipping our members with the knowledge and confidence to address this asset responsibly and collaboratively." - John Wheeler, NAIFA President-Elect.

Equifax Has to Modify VOIE Agreements: NMN

The credit reporting agency is being sued over its VOIE business, The Work Number. The judge called out legal maneuvers and moves he called, “too clever by half.”

Move Over New Day: Veteran’s United is Now in Legal Crosshairs - NMN

The lawsuit is on behalf of 3 veterans who thought Veterans United was representing itself as part of the government. Claims are about deceiving and steering.

MOVING & SHAKING

Big Move from One of the Big Guys: Rocket EVP Mike Fawaz announced on LinkedIn that he's "stepping away" from Rocket Pro after 15 years and says his "next chapter begins with purpose." Fawaz indicated that "more will come soon."

HUD announced the appointment of 6 industry professionals to its Manufactured Housing

Consensus Committee, saying the move maintains the member level required by statute and will help modernize the HUD code for standards and safety in this housing category which is critical to helping increase supply and address affordability for consumers.

RE/MAX promoted Chris Lim to President adding to his existing role of Chief Growth Officer. Also joining the REMAX World Headquarters team are two key leaders in the franchise sales organization: Pierre Montagna as Vice President of Global Sales and Lisa Sennstrom as Director of Global Sales.

Guaranteed Rate Affinity promoted Kevin Ginsburg to national builder division manager.

Ownwell raised $50M, launched national service to streamline property tax appeals in an effort to help make homeownership more affordable.

National Mortgage Insurance Corporation appointed Renu Agrawal to its BOD.

Brokers First Funding appointed Frank Nese and Lito Gonzales to senior sales leadership posts to drive non-QM growth. - NMP

Evergreen Home Loans appointed Dana Klarr as area manager in Arizona to drive growth in the southwest region.

MARKET/INDUSTRY

A Special Treat for InGeniusly Speaking Subscribers: Bill Bodnar shares the market lowdown in his

MMG Minute. Here’s a peek at what the Tabrasa team provides their audience every day.

Flirting with the Fives: Freddie 2-19-26

Mortgage rates dropped again this week, now down to their lowest level since September of 2022. This lower rate environment is not only improving affordability for prospective homebuyers, it’s also strengthening the financial position of homeowners. Over the past year, refinance application activity has more than doubled, enabling many recent buyers to reduce their annual mortgage payments by thousands of dollars.

Mortgage Applications Increased 2.8% from One Week Earlier: MBA Weekly Survey for the week ending 2-13-26.

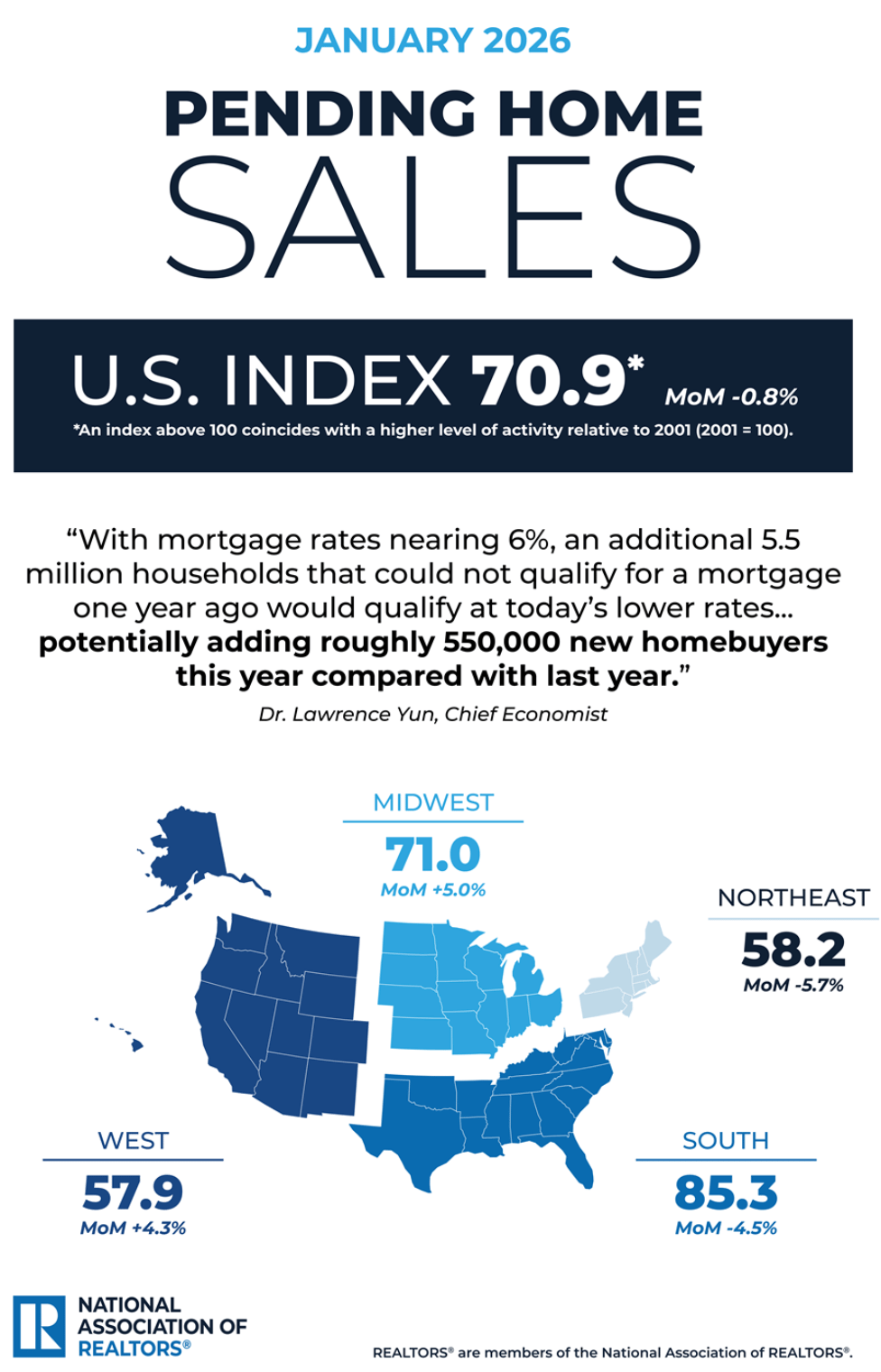

NAR January Pending Home Sales

Month Over Month

0.8% decrease in pending home sales

Gains in the Midwest and West; declines in the Northeast and South

Year Over Year

0.4% decrease in pending home sales

Gains in the South and West; declines in the Northeast and Midwest

“With mortgage rates nearing 6%, an additional 5.5 million households that could not qualify for a mortgage one year ago would qualify at today’s lower rates. Most newly qualifying households do not act immediately, but based on past experience, about 10% could enter the market—potentially adding roughly 550,000 new homebuyers this year compared with last year.” – NAR Chief Economist Lawrence Yun

Beleaguered Builders

Scattered Sentiment: NAHB/WF Housing Index Finds Builders Have Inconsistent Attitudes

The NAHB/Wells Fargo Housing Market Index (HMI) is based on a monthly survey of single-family builders who are asked to rate three specific conditions of the housing market:

Present sales of new single-family homes

Expected sales of single-family homes for the next six months

Traffic of prospective buyers of new single-family homes

Current results:

Builder confidence in the market for newly built single-family homes fell one point to 36 in February. Here are the readings for the three HMI indices in February:

Current sales conditions held steady at 41.

Sales expectations in the next six months fell three points to 46.

Traffic of prospective buyers dropped two points to 22.

It’s interesting to compare attitudes during different times:

April 2020 – 30 (Throes of pandemic)

November 2020 – 90 (The property grab attributed to pandemic)

December 2022 – 31 (“Inflation Reduction Act” passed 8-22)

July 2023 – 56 (Not clear why they got so optimistic here; bad news was coming…)

November 2023 – 30( The month after rates shot up to 7.79%)

Lowdown: Buyer Down Payment Size Shrinks 1st Time in 5 Months

Redfin analysis of county records across 38 of the most populous U.S. metropolitan areas, data is from December 2025, down payment data is limited to home purchases for which buyers took out a mortgage.

The median home sale price rose slightly in December (0.5%) but down payments fell in dollar terms partly because the typical homebuyer put down a lower percentage of the purchase price than a year earlier.

In percentage terms, the typical homebuyer put down 15.2% of the purchase price, compared with 16.7% a year earlier.

Comparison from NAR’s 2025 Profile of Home Buyers & Sellers:

In 2025, the median down payment among all buyers was 19 percent, 10 percent for first-time home buyers, and 23 percent for repeat buyers.

This is the highest down payment for first-time buyers since 1989 and the highest down payment for repeat buyers since 2003.

Fewer All Cash Sales: Redfin's Real Time Report

Just under 3 in 10 (29%) U.S. homebuyers paid in all cash in December, down from 30.3% a year earlier and the lowest December share since 2020. (From NAR 2025 Profile of Home Buyers & Sellers: 26% of home buyers paid cash for their home, continuing an all-time high for all- cash buyers.)

Confusion and Concern: LERETA's 3rd Annual Borrower Escrow Survey

The survey found that 61% of borrowers say they completely understand how a mortgage escrow account works, indicating perceived familiarity even as misunderstandings persist.

62% have experienced payment increases driven by higher property taxes

40% would not be able to make their monthly payment if it increased by 25%

More Bank Buzz from Urban Institute

Urban Institute on the FHL Bank System

The Community Home Lenders of America says IMBs originated 84% of all single-family loans last year. After Fed Gov Michelle Bowman spoke to bankers about wanting banks to do more mortgages, we see this piece from the entitled, “The Value of the FHLBank System to Promote Housing and Community Development Lending.” Key findings:

FHLBank advances are strongly associated with higher lending across banks and credit unions.

Lending responses are strongest in residential real estate.

10 States with Highest Foreclosure Rates

Highest Foreclosure Rate States: ATTOM Data’s January Report

1 Delaware, 2 Nevada, 3 Florida, 4 South Carolina, 5 Maryland, 6 Illinois, 7 Indiana, 8 New Jersey, 9 Utah, 10 Arizona.

What’s “The Bill Pay Economy?” doxo Explains

The 2026 U.S. Household Bill Pay Report found that the typical consumer spends $39,468 per year on household bills, with $24,997 spent on the thirteen most essential household bills. In total, The Bill Pay Economy™ accounts for $5.03T in 2026.

The company says mortgages are $1.08T of the total, while rents are $740B.

Renter Relief: Realtor.com Says It’s a Renter's Market

Vacancy rates have tipped to favor renters and rent increases have continued to moderate.

Numbers Differ, Point is the Same: Zillow Forecasts Rent Moderation Throughout 2026