- InGeniusly Speaking

- Posts

- All In on AI

All In on AI

By Jeff Walton & Kelly Guest

Table of Contents

Whether they're rolling it out, partnering to create it, or using it to write email, everyone is getting on the AI bandwagon. ICEannounced it has several AI agents for servicing in beta testing last week at its event in Vegas, and AI platform Palantir announced a partnership with tech outsourcer Moder to "co-build an AI-powered mortgage operations platform with first pilot customer Freedom Mortgage."

Perhaps most interestingly, Columbia University and Tidalwave conducted a benchmark test pitting general purpose AI against AI that was "fed" with GSE and other underwriting and industry guidelines - story below.

CHATTER

Judge says Nope to FinCEN

Texas Judge Quashes FinCEN Anti-Money Laundering Rule - HW

A federal judge in Texas has vacated the Financial Crimes Enforcement Network’s(FinCEN) nationwide anti-money laundering rule requiring title insurance companies to report details of millions of residential real estate transactions. The judge said FinCEN exceeded its statutory authority with the rule that took effect 3-1.

Saucy Words from FHFA

GSEs Lighten Up on Insurance - FHFA’s Orders

The outspoken FHFA Director Bill Pulte announced the rules in a series of colorful statements, including, “The changes fix expensive, stupid Biden-era requirements with simple, common-sense updates that respond to today’s skyrocketing insurance prices.” Pulte says the new rules for Fannie and Freddie will “[replace] a disruptive and expensive Biden insurance mandate with commonsense policies for today’s market.”

MBA Chief Econ Fratantoni on the Fed:

“Mortgage rates have moved up about a quarter percentage point in recent weeks as longer-term interest rates accounted for the increase in inflation and hence the reduction in the chance that Fed would cut further this year. We forecast that mortgage rates will range between 6% and 6.5% this year, and our latest weekly data show it’s trending towards the upper end of that range.”

IMBs Still Show Profit in Q425, Not as Much as Q3: MBA

The average pre-tax production profit was 17 basis points (bps) in the fourth quarter of 2025, compared to a profit of 33 bps in the third quarter of 2025. The average quarterly pre-tax production profit, from the first quarter of 2008 to the most recent quarter, is 39 basis points.

The average production volume was $643 million per company in the fourth quarter, up from $634 million per company in the third quarter. The volume by count per company averaged 1,973 loans in the fourth quarter, up from 1,866 loans in the third quarter.

Total production revenue (fee income, net secondary marketing income, and warehouse spread) decreased to 340 bps in the fourth quarter, down from 359 bps in the third quarter. On a per-loan basis, production revenues decreased to $11,776 per loan in the fourth quarter, down from $12,310 per loan in the third quarter.

Total loan production expenses – commissions, compensation, occupancy, equipment, and other production expenses and corporate allocations – decreased to 323 basis points in the fourth quarter from 326 basis points in the third quarter. Per-loan costs decreased to $11,102 per loan in the fourth quarter, down from $11,109 per loan in the third quarter. From the first quarter of 2008 to last quarter, loan production expenses have averaged $7,846 per loan.

Including all business lines (both production and servicing), 68 percent of the firms in the report posted pre-tax net financial profits in the fourth quarter, down from 85 percent in the third quarter.

MBA & Others Have Been Advocating for This…

Federal Regulators requested comment on three proposals to modernize the regulatory capital framework for banks of all sizes. The proposals would streamline capital requirements and better align regulatory capital with risk while maintaining the safety and soundness of the banking system.

Dueling Robots: Columbia U and Tidalwave Put AI to the Test

Loan officers across the U.S. are already using general-purpose AI tools. But until now, no public benchmark has measured whether the AI tools lenders are adopting actually produce accurate answers on the questions that matter for loan quality. This study is the first to put a number on that gap. The gap exists because general-purpose models process a loan file as raw text.

Tidalwave is “fed” with Fannie/Freddie and other underwriting/industry guideline info, Claude is not – it’s general AI:

Reverse Seconds Expand

FAM Expands “Reverse Second” – Now in 16 States

HomeSafe Second, the industry’s first second-lien reverse mortgage product in market, has expanded to Indiana, Ohio and Michigan, bringing total availability to 16 states

HomeSafe Second enables homeowners 55+ to turn their home equity into cash without adding a new monthly mortgage payment, while preserving their existing low-rate primary mortgage

Get Money if You Get with the Program: PenFed Home

PenFed launched PenFed Home – a platform that the company says will “bring together mortgage solutions and a trusted network of real estate agents to help homebuyers find, finance and save.”

The press release says buyers can get generous closing cost credits including loan origination fee, appraisal fee, tax service fee, flood certification fee, credit report fee, soft credit report fee, etc. – IF they use the “qualified PenFed real estate network agent assigned to them.”

The announcement for the program also warns that, “Credits may be reduced if all credits received, including seller credits, have reached the maximum allowable credit limit for the selected loan product.”

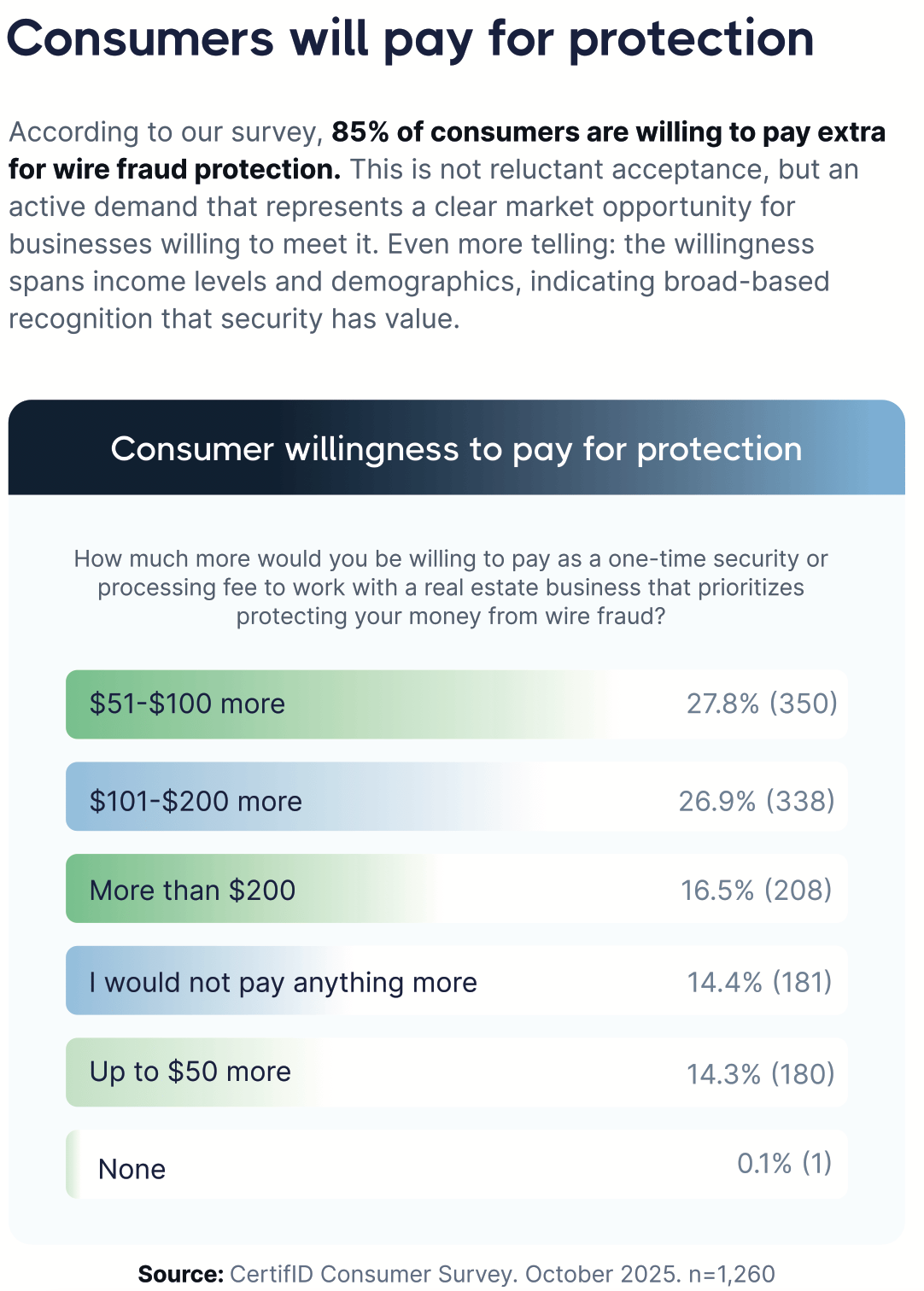

Why Should Only Criminals Get to Profit from Wire Fraud? CertifID 2026 State of Wire Fraud Report

The report basically suggests RE/title companies turn wire fraud protection into a profit center based on the following:

MOVING & SHAKING

CrossCountry Acquired Summit:

"After running a private mortgage bank for over 30 years, I know that growth doesn't happen by accident. It happens through scale, investment and a commitment to supporting the teams out in the field every day." - Todd Scrima, CEO, Summit Funding, Inc. Terms of the acquisition remain confidential.

Onity Group rebranded two companies – PHH Mortgage and Liberty Reverse Mortgage are now under the Onity Mortgage name.

A New Suitor on the Scene

The Two Harbors Board of Directors received an unsolicited proposal to acquire all of the outstanding shares of TWO common stock for $10.70 per share in cash. In addition to the per share cash consideration, the unsolicited proposal provides for the payment of the $25.4 million termination fee that TWO would be required to pay to UWM Holdings Corporation to terminate TWO’s previously announced merger agreement with UWMC. The Committee has not made a determination as to whether the unsolicited proposal is superior to the UWMC transaction.

The parent company of Freedom Mortgage executed an agreement to agreement to acquire Seneca Mortgage Servicing LLC and related entities from EJF Capital LP.

ServiceLink Expands Origination Sales Team - NMP

MARKET/INDUSTRY

A whole lot of chatter going on: Who knew that someone who admits his chairmanship is transitory could rattle the markets? Bill Bodnar addresses last week's Fed events and what to watch in his latest Master the Markets segment.

Average 30-Year Fixed-Rate Mortgage at 6.22%: Freddie 3-19-26

Mortgage Applications Decreased 10.9% from One Week Earlier: MBA Weekly Survey for the week ending 3-13-26.

The MBA’s (BAS) data for February 2026 shows mortgage applications for new home purchases increased 0.9% from a year ago. Compared to January 2026, applications decreased by 1%.

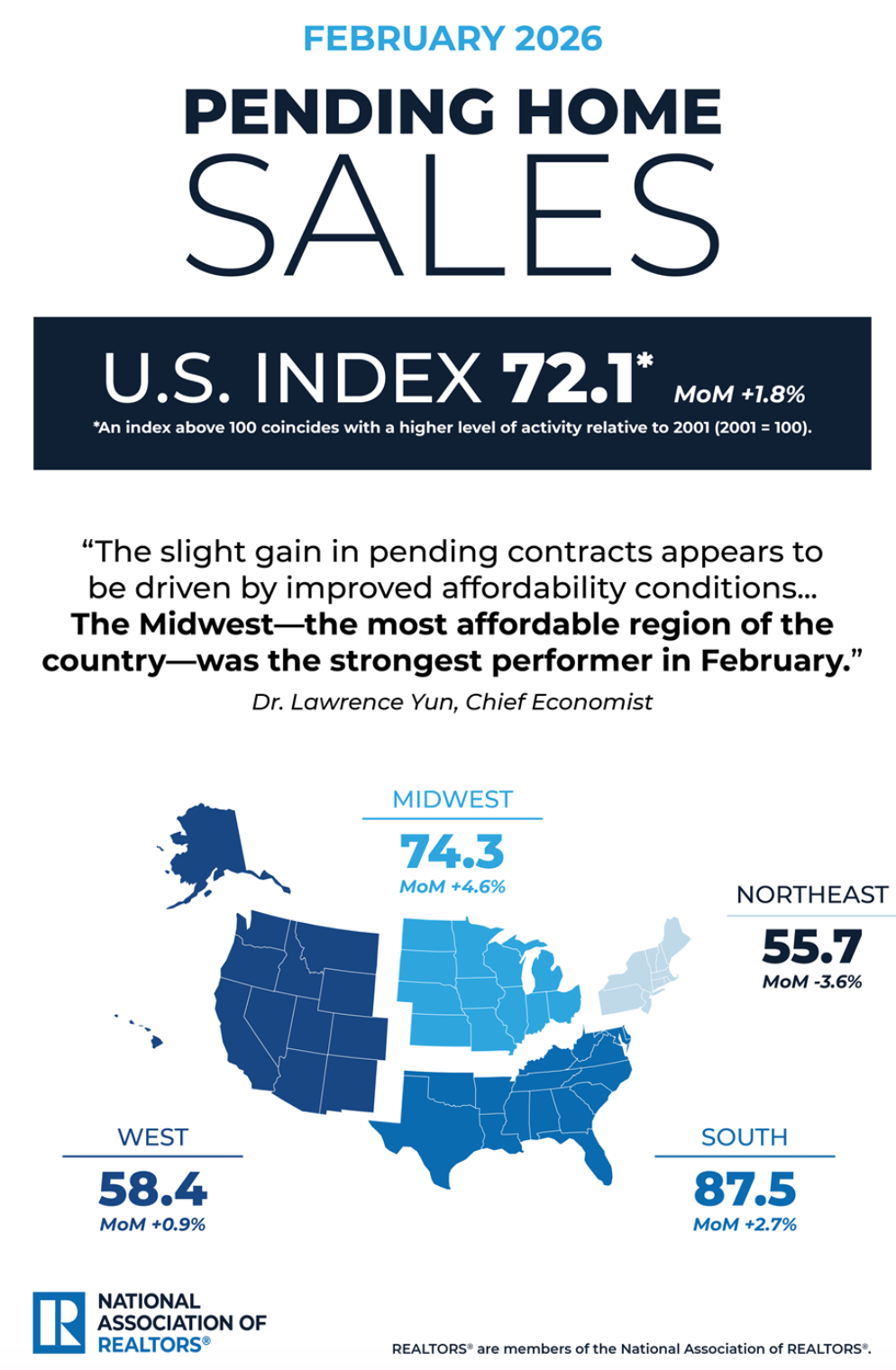

Pendings Perk Up: NAR

Month Over Month:

1.8% increase in pending home sales

Gains in the Midwest, South and West; declines in the Northeast

Year Over Year

0.8% decrease in pending home sales

Gains in the South and West; declines in the Northeast and Midwest

“The slight gain in pending contracts appears to be driven by improved affordability conditions. However, those conditions could reverse if higher oil prices lead to an uptick in mortgage rates.” - NAR Chief Economist Dr. Lawrence Yun.

Damn DOM Up YoY: Redfin

In February 2026, there were 1,717,801 homes for sale in the United States, down 0.56% year over year. The number of newly listed homes was 470,988 and down 5.2% year over year. The median days on the market was 66 days, up 9% year over year. The average months of supply is 4 months, up 0 year over year.

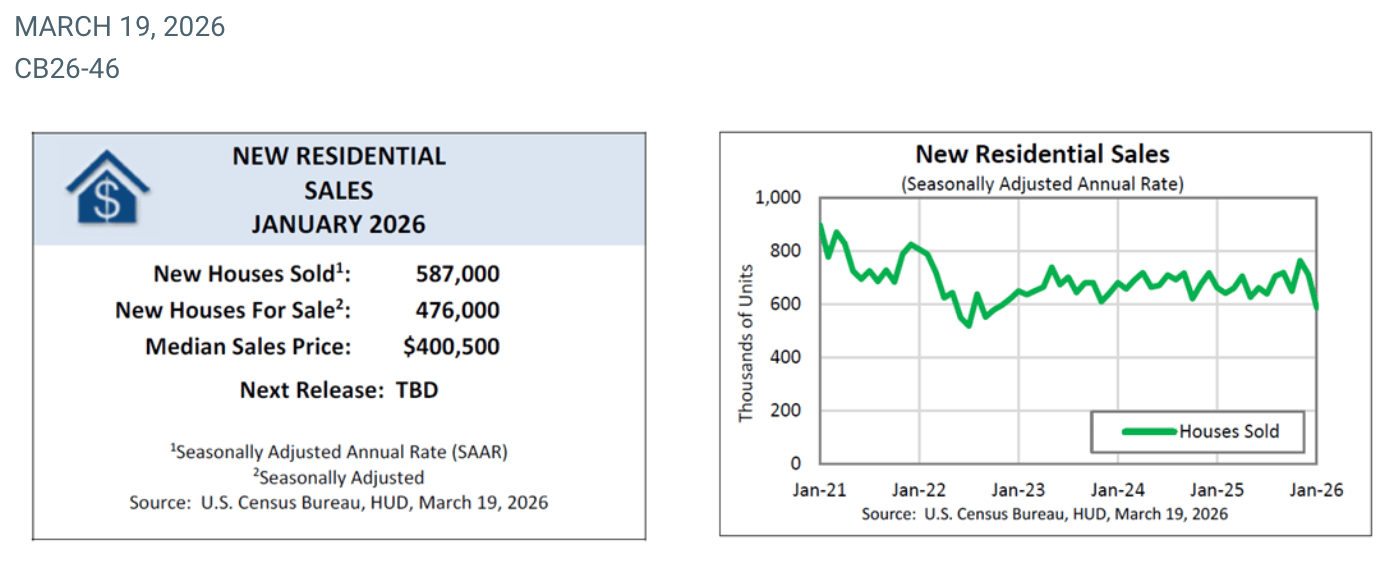

Not a Lot of New Home Sales: US Census/HUD

January new home sales were down 17.6% MoM and 11.3% YoY.

It’s Flippin’ ’08 Again

Flips Fizzled: ATTOM Data’s YE25 Flipping Report

Returns fell to their lowest level since the Great Recession:

A total of 297,045 homes were flipped in 2025, down nearly 4% from the previous year and the lowest annual count since 2020.

Flips made up 7.4% of all home sales, continuing a slight decline from 2024.

ROI fell to 25.5%, the lowest level since 2008, and typical gross profit dropped to $65,981, down from $77,000 last year.

Profit margins declined in 70% of metro areas analyzed.

Foreclosures Down MoM, Up YoY: ATTOM Data Feb Stats

Total filings: 38,840 properties with default notices, scheduled auctions, or bank repossessions

Monthly change: Down 4 percent from January 2026

Year-over-year change: Up 20 percent from February 2025

National rate: One in every 3,701 housing units had a foreclosure filing

States with the worst foreclosure rates: Indiana, South Carolina, Florida, Delaware, and Illinois

Doctor in the House: KBRA Report Says Medical Professional Mortgages are Mainstreaming

The gated report suggests MPMs are a new niche in RMBSs.