- InGeniusly Speaking

- Posts

- Love Letters

Love Letters

By Jeff Walton & Kelly Guest

Lawmakers in Washington had a different Valentine’s Day agenda than most of the rest of us: Letters exchanged between dueling parties and policy priorities were S-H-U-T-D-O-W-N. Norway is eating the world’s lunch at the winter Olympics, but Italy is stepping up on its home turf. Stateside, the banter between the CFPB and the GAO sounds a lot like the dialogue at a curling match between Canada and Sweden.

Table of Contents

CHATTER

Bipartisan? Really??

Just Say Yes: MBA Applauds House Passage of HR644, Tells Senate to Get it Through

House passes Housing for the 21st Century Act on a bipartisan basis. MBA statement snippets:

“This legislation advances several core MBA priorities, including regulatory modernization, broader FHA multifamily financing, stronger rural housing programs, and better coordination across federal housing agencies. Many of these provisions also mirror the Senate’s ROAD to Housing Act, reflecting broad, bipartisan consensus in both chambers that housing affordability action is needed.

“We now urge the Senate to move swiftly and pass its bipartisan ROAD to Housing Act so that leaders in both chambers can reconcile their packages and send a landmark housing affordability measure to President Trump for signature as soon as possible.” - MBA's President and CEO Bob Broeksmit, CMB

MBA on the Jobs Report:

“The January jobs report shows modest improvement relative to prior months. However, the job gains continue to be focused in just a few sectors, matching the uneven pace of economic growth we are seeing in many data releases. Overall, this report provides support for FOMC officials who have voted to keep rates steady for the time being.

“From a housing market perspective, a stronger job market should improve consumer confidence and support demand this spring." - MBA SVP and Chief Economist Mike Fratantoni

CPI Up .2% in January, 2.4% YoY

The index for shelter rose 0.2% in January and was the largest factor in the all items monthly increase. The food index increased 0.2% over the month as did the food at home index, while the food away from home index rose 0.1%. These increases were partially offset by the index for energy, which fell 1.5% in January.

GSEs in the Money

Fannie Mae Earns $3.5B in Fourth Quarter, $14.4Bin 2025

• Net worth grew to $109.0 billion at the end of 2025, up $95.5 billion since the start of 2020

• $141 million reduction in non-interest expenses from 2024, including a $40 million reduction in administrative expenses

• Net revenues stable on quarterly and annual basis at $7.3 billion and $29.0 billion, respectively

• 14 straight years of annual profitability reflect effective long-term risk management and focus on mission

Freddie Mac announced Q425 financial results:

$2.8B in net income

$5.8B in net revenues

$70B net worth

$3.7T total portfolio

Judge Allows Racial Equity Mortgage Program to Continue in WA State - NMN

Who’s Zumper?? ChatGPT Users Will Know…

Zumper, one of the largest privately owned rental marketplaces in North America, today announced the launch of its new rental search app within ChatGPT, giving renters the ability to find available homes and access real-time market insights through conversation.

Watching the Watchdog: GAO Report on CFPB Restructuring Efforts

Between February and August 2025, the Consumer Financial Protection Bureau took multiple actions to reorganize its operations and activities, largely in response to executive orders.

We found that these actions included issuing stop-work orders; closing supervisory examinations; and terminating employees, contracts, and enforcement cases. Some of these actions are subject to ongoing litigation.

CFPB expressed concerns with the accuracy of this report. GAO stands by the accuracy of the facts presented, as discussed in the report.

MOVING & SHAKING

Pennymac announced it has entered into a definitive agreement to acquire the subservicing business of Cenlar Capital Corporation (Cenlar), primarily consisting of subservicing contracts and mortgage servicing operations, in an all-cash transaction for an upfront purchase price of $172.5M and up to $85M of contingent consideration payable over three years.

Planet Home Lending added John Rinaldi and Paul Butuc as regional sales managers in Northeast.

Waterstone Mortgage announced multiple promotions: Casey Seefeldt, VP – Capital Markets, Melissa Wagner, PHR, VP – HR, Scott Howard, Director – Information Security, Zach McCarthy, Director – Financial Planning & Analysis.

Visio Lending named Mimi Frusha as CFO.

Altisource welcomed Rick Seehausen as President of Lenders One Mortgage Cooperative.

MARKET/INDUSTRY

Good Data: Bill Bodnar explains the good tailwinds for the mortgage industry as we head into the winter thaw in his latest Master the Markets segment.

Mortgage Rates Inch Down: Freddie 2-12-26

Mortgage Applications Decreased 0.3% from One Week Earlier: MBA Weekly Survey for the week ending 2-6-26.

Seasonal Slump, Refis Rev: ATTOM Data Q425 US Residential Originations Report

Refinance loans rose 6% quarter-over-quarter and 11% year-over-year, accounting for 42.6% of all originations, surpassing purchase loans for the first time in nearly four years.

Home purchase mortgages fell 14% from the prior quarter and 13% from a year earlier, reflecting ongoing affordability pressures and seasonal slowdown.

Despite fewer loans issued, total mortgage dollar volume increased 1% from Q3 and 4% year-over-year, reaching $627.3 billion.

Home equity lending declined quarter-over-quarter but rose 9% from a year ago, signaling continued homeowner interest in tapping equity despite broader lending shifts.

Back to Balance: Cotality February Home Price Index

“We are seeing a significant departure from the rapid surges of recent years; while the upward pressure on prices remains, the momentum has moderated enough to suggest that the market is finally becoming more navigable for prospective buyers.”

“As we move through 2026, the market’s trajectory will depend heavily on wage growth and how soon buyers regain the purchasing power needed to meet sellers’ pricing thresholds. For now, Cotality data shows a housing landscape is still finding its footing, but it is ultimately stabilizing after an extended period of imbalance.” - Cotality Chief Economist Dr. Selma Hepp.

More Than Sales Numbers…

Reevaluating the Market: 1st Am Has Different Way to Assess Market

Housing activity is often evaluated by comparing today’s sales totals to those from years past. But raw sales counts can be misleading when the market itself has grown. The total number of U.S. households, which represents the demand for shelter, has steadily increased over time. In 2025, there were 135 million households, compared with 118 million households fifteen years ago, an increase of roughly 15 percent. So, an annual pace of 4 million existing-home sales today represents considerably less activity, relative to demand, than fifteen years ago.

The housing market is recovering, but we are still far from where a market of this size and demand should be. Instead, it reflects a market that is loosening after an extended period of constraint. A more durable recovery in sales activity is likely to come gradually, as time and life events begin to outweigh financial inertia. Job changes, family transitions, downsizing, retirement, and relocation will continue to bring homes to market, even if mortgage rates remain elevated. Indeed, 47 million Americans are in their thirties, and many still rent, representing a large pool of potential first-time buyers that may trickle into the market as life stages slowly line up with housing needs.

Interesting Insights: ICE 2-26 Mortgage Monitor

Refinance incentives surged to a nearly four-year high following early-January interest rate declines

Housing affordability reached its best level since early 2022, but remains stretched by historical standards

Negative equity is increasing modestly, concentrated in recent vintages and select Southern markets

Home price growth slowed to its weakest pace in more than a decade, with regional divergence widening

Drowning in Debt?

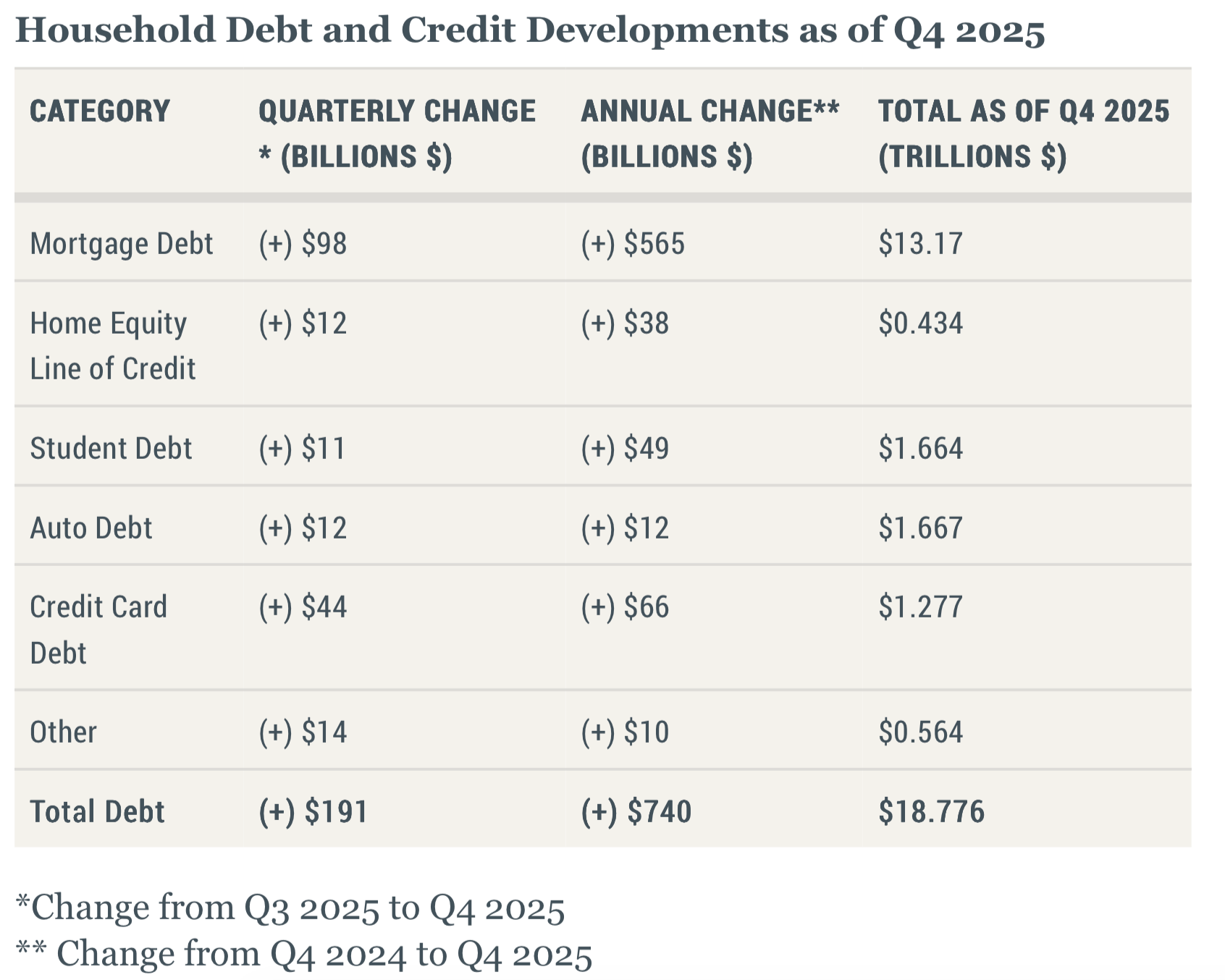

Damn Debt: NY Fed Q425 Household Debt Report

US household debt jumped $549B YoY from Q424 to Q425!

Wait – there’s more:

Mortgage balances grew by $98 billion in the fourth quarter and totaled $13.17 trillion at the end of 2025. Credit card balances rose by $44 billion and stood at $1.28 trillion.

Auto loan balances increased by $12 billion to $1.67 trillion, after holding steady during the prior quarter.

Home equity line of credit (HELOC) balances increased by $11.6 billion to $434 billion while student loan balances rose by $11 billion to $1.66 trillion.

Non-housing balances rose by $81 billion, a 1.6% increase from Q3 2025.

Another Affordability Indicator: Redfin Says Buyers Need 4% Less to Get In YoY

Homebuying affordability is improving nationwide after nearly five years during which it generally worsened. That’s because mortgage rates are lower and home-price growth is muted.

Affordability is improving in 37 of the 50 most populous U.S. metro areas.

Americans need to earn $111,252 per year to afford the typical U.S. home for sale, down 4% from $115,870 a year ago.

The income needed to buy a home has been declining since November, providing some much-needed relief for U.S. homebuyers. Before that, the income needed to afford a home had been rising on a year-over-year basis nearly every month for five years straight, since the pandemic homebuying boom drove up home-sale prices. The income needed to buy a home peaked at over $122,000 this past June.

Are Seniors Getting Screwed?

Older Selles Get Less Money: Boston College Paper

Older sellers receive lower returns because: 1) their homes have poorer upkeep; and 2) they more often sell on private listings and sell to investors.

The negative relationship between a home seller’s age and annual returns is large. An 80-year-old seller realizes about 0.5 percent per year less than a 45-year-old, which corresponds to a 5-percent-lower sales price for a home with the mean holding period (11 years). On the typical home price of $400,000, this reduction amounts to a loss of $20,000.

Fueling Foreclosures: ATTOM Data January 2026 U.S. Foreclosure Market Report

Foreclosure filings were up 32% from January 2025 even as activity dipped 10% from December.

Foreclosure starts rose 26% annually, while completed foreclosures (REOs) increased nearly 59% from a year ago.

FHA Delinquencies Up; Relief Options Expired

The delinquency rate for mortgage loans on 1-4 unit residential properties increased to a seasonally adjusted rate of 4.26% of all loans outstanding at the end of Q425, according to the Mortgage Bankers Association’s (MBA) National Delinquency Survey.

“The fourth quarter results may have been impacted by the expiration of pandemic-era, FHA relief options as well as disparities in the labor market – a key determinant of mortgage delinquency levels.” - Marina Walsh, CMB, MBA’s Vice President of Industry Analysis.