- InGeniusly Speaking

- Posts

- Oil Slick

Oil Slick

By Jeff Walton & Kelly Guest

A lot of industry experts used words like wild and crazy to describe last week. Higher oil prices offset both safe haven trade into bonds and even the lousy jobs report that would normally help rates. Bill Bodnar broke the rate situation down in his latest Master the Markets segment, while HW's Logan Mohtashami chimed in noting, "with all the drama last week, it was a pretty normal housing week. Housing data showed year-over-year growth, weekly pending home sales rose, inventory declined slightly and mortgage rates were very steady, considering the conflict with Iran.”

Table of Contents

CHATTER

Robo-Approval?! Better.com Announces First Conversational Credit Decision Engine in ChatGPT

The company announced the launch of the first conversational credit decision engine for mortgages and home equity loans in ChatGPT with OpenAI.

"The mortgage industry is riddled with inefficiencies that hurt consumers, as well as the loan officers and lenders who serve them. Big mortgage aggregators in the broker and correspondent channel charge what is essentially a 1-2% tax on each loan just to underwrite a mortgage and deliver it to an institutional investor. That ends now. Loan officer teams and banks can simply log into their ChatGPT Enterprise account, download the Tinman AI credit decision engine app, connect their guidelines, pricing, and CRM to process, underwrite, and fulfill loans nearly instantly, passing thousands of dollars in savings to consumers. We’ve put the full power of Tinman inside ChatGPT, a platform more than 100 million Americans already know and trust. This is a total game changer." - Leah Price, General Manager of Tinman AI Platform.

Itchy Trigger Fingers Beware

No Mas Trigger Leads: Homebuyers Privacy Protection Act in Effect 3-5-26

The law amends the Fair Credit Reporting Act (FCRA) to prohibit consumer reporting agencies from furnishing mortgage trigger leads except in narrowly defined circumstances.

Under the new law, a trigger lead may only be generated if the requesting creditor already has a qualifying existing relationship with the consumer — such as an active mortgage loan or a deposit account — or if the consumer has affirmatively opted in to receiving such solicitations.

Any permissible trigger lead must also be used for a bona fide firm offer of credit or insurance, not simply as a marketing hook.

The law amends the Fair Credit Reporting Act (FCRA) to prohibit consumer reporting agencies from furnishing mortgage trigger leads except in narrowly defined circumstances.

Under the new law, a trigger lead may only be generated if the requesting creditor already has a qualifying existing relationship with the consumer — such as an active mortgage loan or a deposit account — or if the consumer has affirmatively opted in to receiving such solicitations.

Any permissible trigger lead must also be used for a bona fide firm offer of credit or insurance, not simply as a marketing hook.

Do we need insurance on our insurance?

Insurance is an Issue: Premiums & Uninsurability Up - NRDC

The average homeowner has seen increases of 24% between 2021 and 2024.

Insurers have been increasing deductibles to transfer some of the financial risk from the insurer to policyholders.

The average insurance deductible increased by 15% from 2023 to 2024 and by 24.5% from 2024 to 2025.

Manufactured Boom: I’m HOME Manufactured Housing Industry Benchmark Report

The Lincoln Institute of Land Policy’s Innovations in Manufactured and Modular Homes Network released its 2nd annual report, claiming that manufactured housing production in the US increased in 2024, and touting it as a cost-effective, streamlined approach to addressing the country’s severe housing shortage and lack of affordable housing.

The GSEs have made increasing efforts to back financing for this housing sector.

MOVING & SHAKING

Fairway Home Mortgage promoted Holly Mattson to Co-President of Recruiting where she will oversee Fairway's efforts to onboard top mortgage producers.

Cotality appointed former USAA CEO Wayne Peacock to its board.

CrossCountry Mortgage welcomed Nicole Rueth as Senior Vice President in the Denver market.

Nicole Lamorte joined Nations Lending as branch manager in Crystal Lake, IL.

Informative Research hired fintech vet Mark Jones to lead partner strategy.

MARKET/INDUSTRY

Mortgage Rates Hold Steady: Freddie 3-5-26

Mortgage Applications Increased 11% from One Week Earlier: MBA Weekly Survey for Week Ending 2-27-26

Spring in our step?

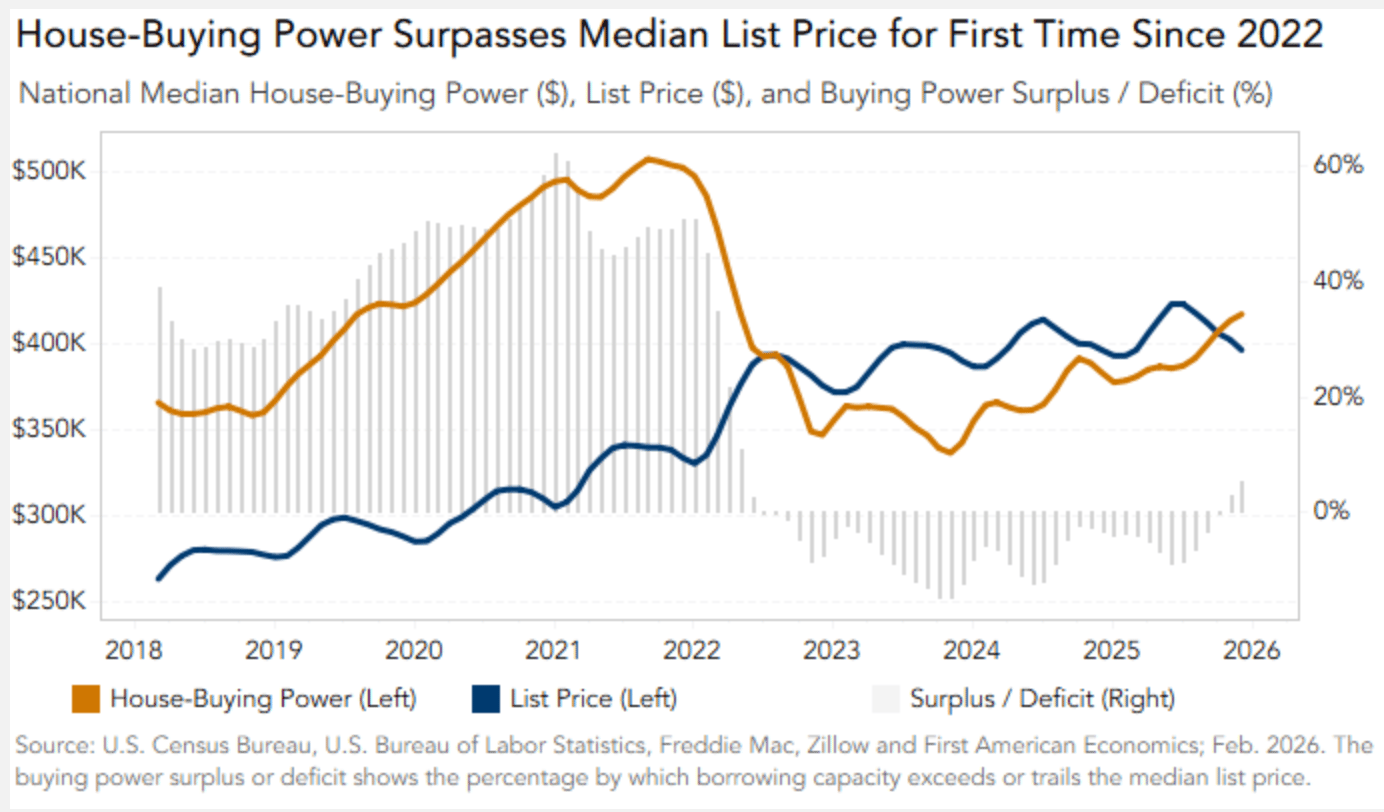

Breaking the Slump: Spring Home Buying Could Get Good - 1st American

“House-buying power reached a significant milestone, surpassing asking prices at the national level for the first time in more than three years.” – 1st Am Sr. Econ Sam Williamson

House-buying power enters the 2026 spring home-buying season above the national median list price for the first time in more than three years.

In December 2025, house-buying power reached $417,000 at the national level, a five percent surplus above the national median list price of $396,000.

While still below pre-pandemic norms, the modest surplus should support a stronger spring sales season than buyers and sellers have seen in recent years.

It’s hardest on the kids…

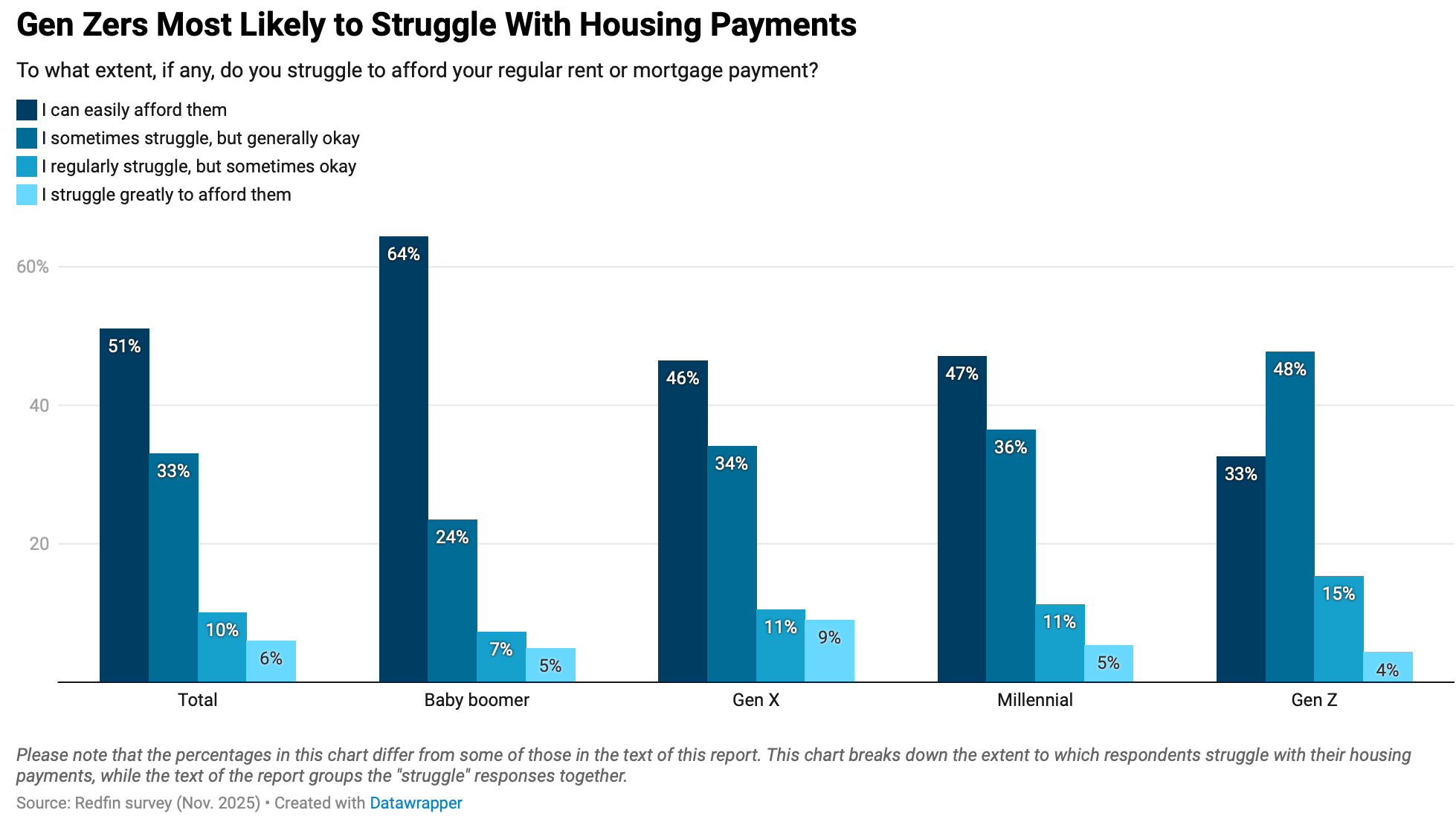

Almost Half the Country Struggles with Housing Payments Redfin/Ipsos

[Poll Conducted in November 2025]

Gen Zers are more likely than older generations to struggle with housing payments. About two-thirds (67%) of Gen Zers struggle to afford their rent or mortgage, compared with just over half of millennials and Gen Xers (53% and 54%, respectively) and 36% of baby boomers.

Well above water…

Many Still Equity Rich: ATTOM Data

In Q425, homeowner equity across the U.S. continued to soften compared to both the prior quarter and the same period last year.

Percentage of Equity-Rich Properties: 44.6% of mortgaged residential properties were considered equity-rich, meaning homeowners owed no more than half of their property’s estimated market value.

Quarter-over-quarter change: down from 46.1% in Q3 2025.

Year-over-year change: down from 47.7% in Q4 2024.

Homeowners Hanging On: Average Tenure is 12 Yrs - Redfin

Homeowner tenure peaked at 13.4 years in 2020, roughly doubling the average tenure from 2005.

Then it declined marginally for four years before ticking up in 2025.

People hanging onto their houses can be an obstacle for first-time homebuyers because it limits inventory and pushes up prices.

Tenure is longest in California, largely because state tax laws incentivize homeowners to stay put. In Los Angeles, the typical homeowner hangs onto their house for 20 years, followed by San Jose, where it’s nearly 19 years.

Tenure is shortest in relatively affordable metros, led by Louisville and Las Vegas.

Don’t be CHI: NAHB Cost of Housing Index (CHI)

The CHI represents the portion of a typical family’s income needed to make a mortgage payment on a median-priced home.

CHI results for the fourth quarter of 2025 are based on a national median income of $104,200 and a median new home price of $405,300 (compared to $414,900 for a median-priced existing home). In Q4 2025:

34% of a typical family’s income was needed to make a mortgage payment on a median-priced new single-family home (and 34% for a median-priced existing home).

67% of a low-income family’s earnings would be needed to pay for a median-priced new single-family home (and 69% for a median-priced existing home).

In eight out of 175 markets in the fourth quarter, the typical family is severely cost-burdened (must pay more than 50% of their income on a median-priced existing home).

In 69 other markets, such families are cost-burdened (need to pay between 31% and 50%).

There are 98 markets where the CHI is 30% of earnings or lower.

760 is the Magic Number: AD Mortgage Details the Obvious, Provides Marketing Angles

It’s well known that higher credit scores give borrowers access to better rates and terms. AD Mortgage did a detailed report, and used this benchmark: A FICO score of 760 was chosen as the benchmark for “very good” credit, based on tiers used in the myFICO Loan Savings Calculator, which identifies 760+ as qualifying for the best available mortgage rates.

AD’s report goes on to consider how long it takes for consumers to improve scores and discuss opportunities to educate/nurture.

Rental Returns Dropping: ATTOM Data

Rental yields are declining from 2025 to 2026 in 54.8% (187) of the 341 counties with sufficient data to analyze for both years.

Typical wages increased at a greater rate than three-bedroom rents from 2025 to 2026 in 63% (262) of the 416 counties.

Wages rose at a greater rate than median home sales prices in 66.8% (278) of the 416 counties.

Investor Exits: Parcl Labs Tracking Investor Behavior as DC Threatens Limits on SFR Ownership

The White House is advancing a proposal to ban investors owning 100+ single-family homes from purchasing additional properties. While the policy works its way through Washington, investors aren't waiting. Parcl Labs' investor-mapping technology links true corporate owners to their for-sale listing activity, making it possible to track how they're responding in real time. We analyzed the data:

Investor exits were underway before the Executive Order.

The investor retreat is accelerating.

The 100+ segment the ban would target is already moving.

The biggest institutional landlords are largely on the sidelines.

During the 2020-2021 accumulation years, ratios across these markets regularly exceeded 2.0x, meaning investors bought twice as many homes as they sold. That era is over.

The proposed ban targets investor purchases, not ownership. Investor purchase activity has already been falling since rates rose in 2022, before the current administration took office. The ban would restrict a behavior that the market has been curtailing on its own for years.